IFRS S1 S2 Sustainability Disclosure India

- Harsh Ballyan

- May 4

- 5 min read

ESG & SUSTAINABILITY INSIGHTS | SUSTAIND.IN

SEO META DESCRIPTION

The global language of sustainability reporting is changing rapidly, and India is no exception. IFRS S1 S2 sustainability disclosure India has become one of the most searched and discussed topics in boardrooms, CFO offices, and ESG teams across the country. With the International Sustainability Standards Board (ISSB) having finalised its landmark standards — IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) — Indian companies face a pivotal moment: adapt proactively or scramble to comply later. At Sustaind, we believe that understanding these standards early is not just a compliance strategy — it is a competitive advantage.

What Are IFRS S1 and IFRS S2?

The ISSB, established under the IFRS Foundation, released S1 and S2 in June 2023 with the goal of creating a comprehensive, globally consistent baseline for sustainability-related disclosures. These standards are designed to give investors, lenders, and other capital market participants the information they need to assess risks and opportunities that are material to an organisation's enterprise value.

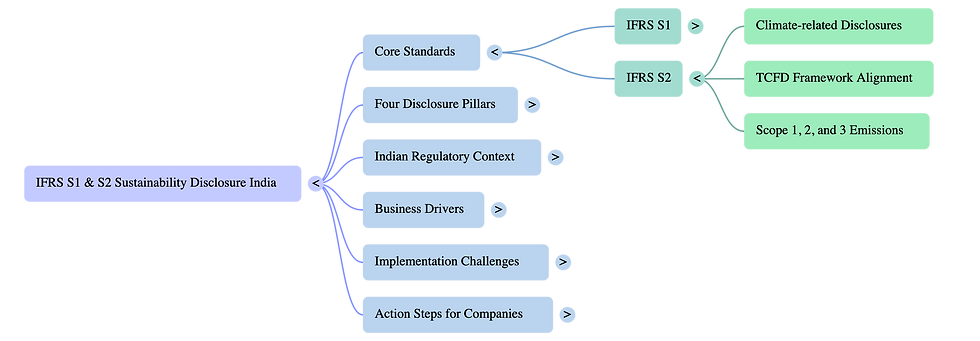

IFRS S1 is the foundational standard. It requires companies to disclose material information about all sustainability-related risks and opportunities — environmental, social, and governance — that could reasonably affect a company's cash flows, financing access, or cost of capital over the short, medium, and long term. Think of it as the overarching framework under which all sustainability disclosures sit.

IFRS S2, building on the foundation of S1, narrows its focus specifically to climate-related risks and opportunities. It is heavily informed by the Task Force on Climate-related Financial Disclosures (TCFD) framework and requires disclosures across four pillars: Governance, Strategy, Risk Management, and Metrics & Targets. Crucially, it mandates companies to report Scope 1, Scope 2, and — where material — Scope 3 greenhouse gas emissions.

Together, S1 and S2 represent the most significant shift in global sustainability reporting in over a decade. For Indian businesses, the question is no longer if these standards will apply — it is when and how.

The India Connection: Where Do Things Stand?

India has been actively engaging with global sustainability reporting developments. The Securities and Exchange Board of India (SEBI) introduced the Business Responsibility and Sustainability Report (BRSR) in 2021, making it mandatory for the top 1,000 listed companies by market capitalisation from FY 2022-23. The BRSR Core, introduced in 2023, took this further by mandating assurance on specific key performance indicators.

However, BRSR and IFRS S1/S2 are not the same beast. While BRSR is India-specific and captures a broad range of ESG metrics aligned to domestic policy priorities, IFRS S1 and S2 are designed for international capital market audiences and focus sharply on financial materiality — the impact of sustainability factors on enterprise value.

SEBI and the Ministry of Corporate Affairs (MCA) are currently examining how India can align its reporting ecosystem with ISSB standards, recognising that Indian companies listed on global exchanges or seeking international investment must speak the language of IFRS sustainability disclosures. Several SEBI consultations have explored interoperability between BRSR and IFRS S1/S2, and Sustaind closely monitors these developments to help clients stay ahead of the curve.

Why IFRS S1 and S2 Matter for Indian Companies

Even if mandatory adoption in India is still being phased in, the practical pressures are already here. Indian subsidiaries of multinational corporations are already being pulled into IFRS S1/S2 disclosures through their parent companies' reporting requirements in Europe, the UK, or the US. Export-oriented businesses, infrastructure companies, and financial institutions are facing ESG due diligence queries from foreign investors and lenders that are directly aligned with ISSB standards.

Here are the key reasons why Indian businesses should start preparing now:

Investor expectations are shifting. Global asset managers — including many who invest in Indian equities — are aligning their portfolio assessment tools with ISSB standards. Clear, comparable sustainability disclosures can directly influence access to capital.

Supply chain compliance pressures. Multinationals are requiring their Indian suppliers and partners to report emissions and ESG data in formats consistent with IFRS S2, particularly for Scope 3 accounting.

Regulatory convergence is inevitable. SEBI and MCA are on a trajectory toward alignment with ISSB. Companies that have already built their data collection and governance structures will transition far more smoothly.

Reputational and competitive advantage. Organisations that voluntarily adopt IFRS S1/S2 aligned reporting signal to global stakeholders that they are serious about sustainability — differentiating themselves in a crowded market.

Key Disclosure Requirements: A Snapshot

For companies beginning their IFRS S1/S2 journey, it is essential to understand the core disclosure elements. Both standards organise disclosures around four interconnected pillars:

Governance: How does the company's board and management oversee sustainability-related risks and opportunities? This includes board-level accountability, management roles, and how sustainability is integrated into strategic decision-making.

Strategy: What are the identified sustainability risks and opportunities, their time horizons, and their impact on the company's business model, value chain, and financial position? S2 specifically requires scenario analysis to test resilience to different climate futures.

Risk Management: How are sustainability-related risks identified, assessed, prioritised, and managed — and how do these processes integrate with the overall enterprise risk management framework?

Metrics and Targets: What quantitative and qualitative information does the company track to measure its performance, and what targets has it set? For S2, mandatory GHG emission reporting using the GHG Protocol is a central requirement.

Sustaind's advisory team specialises in helping Indian organisations map their existing data and governance structures against these four pillars — identifying gaps and building a credible, audit-ready disclosure pathway.

Challenges Indian Companies Will Face

Implementing IFRS S1 and S2 is not without challenges, particularly for organisations new to structured sustainability reporting. Data availability and quality remain the most significant hurdle — especially for Scope 3 emissions, which require engagement across complex, often informal supply chains. Many Indian SMEs and mid-caps lack the internal systems to track granular energy, water, and emissions data at the level of detail ISSB standards demand.

Beyond data, there is a skills and capacity gap. Sustainability reporting under IFRS S1/S2 requires fluency in both financial reporting concepts and ESG measurement methodologies — a combination that is currently rare in India. Companies will need to invest in training, technology platforms, and in some cases, external advisory support to build this capability.

Assurance is another emerging requirement. While ISSB standards do not yet mandate third-party assurance, global investors increasingly expect it — and regulators in multiple jurisdictions are moving toward making it mandatory. Indian companies would be wise to design their disclosures with assurance in mind from day one, rather than retrofitting.

How Sustaind Can Help

Sustaind is India's purpose-built sustainability intelligence platform, designed to help businesses navigate the evolving landscape of ESG reporting and compliance. Whether you are a listed Indian company looking to align your BRSR disclosures with IFRS S1/S2 requirements, a multinational subsidiary managing group-level reporting, or a growing enterprise building your sustainability programme from the ground up, Sustaind provides the tools, frameworks, and expertise you need.

From baseline assessments and materiality analysis to emissions quantification, stakeholder engagement, and disclosure drafting — Sustaind's solutions are built for the Indian context while being globally aligned. Our team stays at the forefront of regulatory developments from SEBI, MCA, and the ISSB, so your organisation never gets caught off guard.

The transition to IFRS S1 and S2 sustainability disclosure in India is not just a compliance checkbox. It is an opportunity to build trust, attract capital, and lead on the sustainability agenda. Sustaind is here to make that transition practical, efficient, and impactful.

Conclusion: Act Now, Not Later

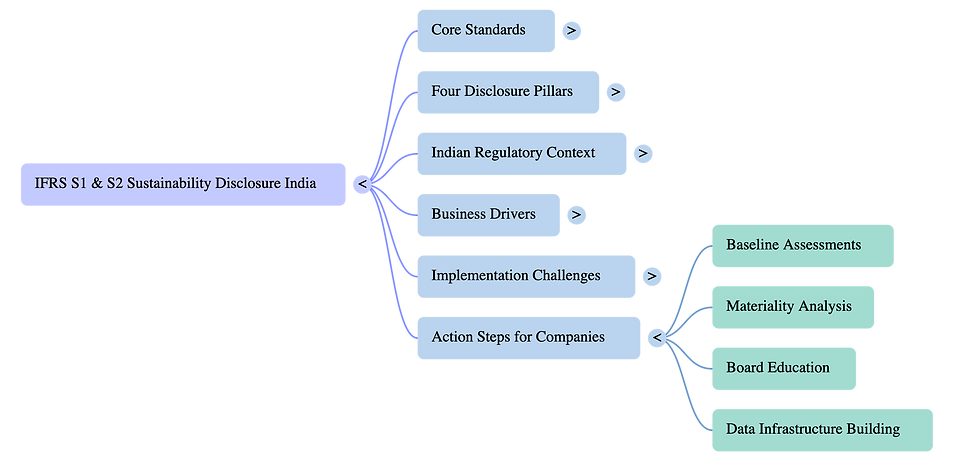

The IFRS S1 S2 sustainability disclosure India conversation is moving from policy circles into mainstream business strategy. The companies that begin their alignment journey today — building data infrastructure, educating boards, engaging supply chains, and drafting disclosures — will be the ones best positioned when mandatory adoption arrives. Sustainability reporting is no longer a back-office function; it is a boardroom imperative.

www.sustaind.in | India's Sustainability Intelligence Platform

Comments