Sustainability Reporting Frameworks India 2026

- Dolly Soni

- May 4

- 4 min read

Sustainability reporting frameworks in India 2026 are no longer a niche concern for multinational corporations or niche ESG enthusiasts — they have become a boardroom imperative. As regulatory expectations tighten and investor scrutiny intensifies, Indian businesses of all sizes are being called upon to measure, disclose, and improve their environmental, social, and governance (ESG) performance. Whether you are a listed company navigating SEBI mandates or an MSME building your sustainability credentials for the supply chain, understanding the reporting landscape is the first step. At Sustaind, we help Indian businesses demystify this landscape and build disclosure practices that are credible, compliant, and future-ready.

Also Read: Sustainability Consulting for SMEs in India

Why 2026 is a Defining Year for ESG Reporting in India

The year 2026 marks a meaningful inflection point. Several mandatory and voluntary frameworks have either come into force or are being significantly upgraded. SEBI's Business Responsibility and Sustainability Report (BRSR) mandate — which became compulsory for the top 1,000 listed companies by market capitalisation from FY 2022-23 — is now maturing, with SEBI introducing the BRSR Core and assurance requirements for the top 150 listed entities. Meanwhile, global standard-setters are converging, and Indian regulators are paying close attention. The pressure is not just regulatory: institutional investors, global buyers, and rating agencies are all asking harder ESG questions than ever before.

For companies that have deferred their sustainability reporting strategy, 2026 is the year to act — not to comply minimally, but to report with intention.

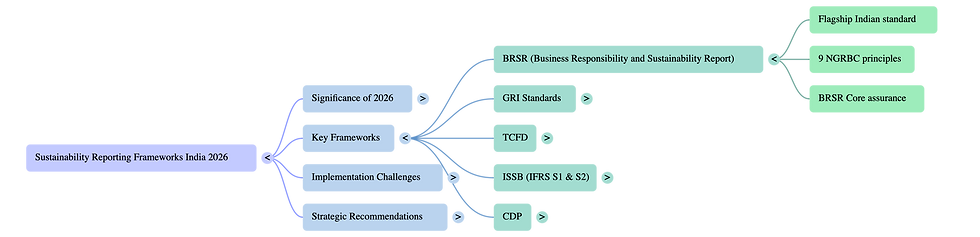

Key Sustainability Reporting Frameworks Relevant to India in 2026

1. BRSR — India's Flagship Disclosure Standard

The Business Responsibility and Sustainability Report (BRSR), introduced by SEBI in 2021, remains the cornerstone of corporate sustainability disclosure in India. Structured around the nine principles of the National Guidelines on Responsible Business Conduct (NGRBC), it covers areas ranging from environmental stewardship and ethical governance to community engagement and responsible supply chains. In 2026, BRSR Core — a subset of high-priority, assurance-ready KPIs — is being progressively extended beyond the top 150 companies. Businesses preparing their BRSR should focus on data quality and internal controls, as third-party assurance is increasingly expected and will become mandatory for a wider cohort.

2. GRI Standards — The Global Benchmark

The Global Reporting Initiative (GRI) Standards remain the most widely used voluntary sustainability reporting framework globally, and Indian corporates with international stakeholders or overseas listings frequently align their reports with GRI. The GRI Universal Standards (GRI 1, 2, and 3), updated in 2021, provide the foundation, while sector-specific standards guide industry-tailored disclosures. Many Indian companies use GRI alongside BRSR through content mapping, recognising significant overlap between the two frameworks. For businesses looking to attract foreign institutional investors or communicate with global value chain partners, GRI alignment adds important credibility.

3. TCFD — Climate Risk Takes Centre Stage

The Task Force on Climate-related Financial Disclosures (TCFD) framework has rapidly moved from a voluntary best-practice to an expectation for large companies and financial institutions. Although TCFD has now been integrated into the ISSB's IFRS S2 standard, its four pillars — Governance, Strategy, Risk Management, and Metrics & Targets — continue to shape how companies articulate climate risk and opportunity. RBI and SEBI have both signalled greater expectations around climate risk disclosure for regulated entities and listed companies respectively. Businesses in carbon-intensive sectors, banking, and insurance should treat TCFD-aligned reporting as a near-term compliance necessity, not a future aspiration.

4. ISSB Standards (IFRS S1 & S2) — The Global Baseline Arrives

The International Sustainability Standards Board (ISSB) released IFRS S1 (General Requirements for Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) in 2023. These are fast becoming the global baseline for sustainability disclosure, with over 30 jurisdictions committing to adoption or reference. India's Ministry of Corporate Affairs and SEBI are actively studying ISSB alignment, and it is widely anticipated that Indian standards will progressively converge with IFRS S1 and S2 over the next few years. Forward-thinking Indian companies — especially those with international capital market access — are well advised to familiarise themselves with these standards now.

5. CDP — Disclosure for the Value Chain

CDP (formerly the Carbon Disclosure Project) is increasingly relevant for Indian companies that are suppliers to large multinationals. Global buyers are requesting CDP scores from their Tier 1 and Tier 2 suppliers as part of Scope 3 emissions management. Disclosing through CDP on climate, water, and forests signals transparency and can directly influence procurement decisions. As supply chain sustainability pressures mount through regulations like the EU Corporate Sustainability Due Diligence Directive (CSDDD), Indian exporters and manufacturers cannot afford to overlook CDP.

Choosing the Right Framework for Your Business

With multiple frameworks in play, the practical challenge is prioritisation. Here is a simple way to think about it:

Listed on Indian exchanges (top 1,000 by market cap)? BRSR is mandatory — start there.

Seeking foreign institutional investment or international listings? Add GRI and/or ISSB alignment.

In a climate-sensitive or financial sector? Integrate TCFD disclosures into your annual report.

Part of a global supply chain? Start your CDP disclosure journey without delay.

The good news is that these frameworks share considerable common ground, particularly around governance, risk management, and environmental metrics. A well-structured sustainability data system can feed multiple frameworks simultaneously, reducing duplication of effort.

Common Mistakes Indian Businesses Make in Sustainability Reporting

Based on Sustaind's experience working with Indian businesses across sectors, a few pitfalls come up repeatedly:

Treating BRSR as a compliance checkbox rather than a strategic communication tool.

Collecting data in silos without a unified ESG data management system.

Ignoring Scope 3 emissions even when global buyers are already asking for them.

Waiting for regulatory certainty before beginning — the landscape will never be fully settled.

How Sustaind Helps You Navigate the Reporting Maze

Sustaind is built for the Indian sustainability context. Our platform and advisory services help companies map existing disclosures to multiple frameworks, identify data gaps, build internal data collection workflows, and produce investor-grade sustainability reports — without the confusion of navigating each framework independently. From BRSR readiness assessments to GRI-aligned reporting and TCFD scenario analysis, we work with Indian businesses at every stage of their ESG journey.

Sustainability reporting is not just about compliance — it is about telling a credible story of long-term value creation. When done well, it builds trust with investors, customers, employees, and communities. In 2026, that story matters more than ever.

Comments