The Future of Agri-ESG: Scaling Carbon Credits in Saudi Arabia’s Agriculture Sector

- Dolly Soni

- May 8

- 5 min read

The future of Agri-ESG and scaling carbon credits in Saudi Arabia’s agriculture sector (Also Read: ESG Advisory Services for Indian Companies) sits at a rare and compelling intersection — where national survival imperatives meet climate ambition, and where arid desert land is being reimagined as a platform for regenerative, low-carbon food production. As the Kingdom accelerates its Vision 2030 transformation, agriculture is no longer a footnote in Saudi sustainability conversations. It is becoming a frontline in the global race to link food systems with carbon markets, green finance, and measurable ESG outcomes.

Why Saudi Agriculture Cannot Afford to Ignore ESG

Saudi Arabia imports close to 80% of its food requirements, spending an estimated SAR 100–120 billion annually on food imports. With arable land covering less than 2% of its territory and renewable freshwater per capita among the lowest in the world, the Kingdom’s agricultural sector has always operated under exceptional constraint. But what once looked like a liability is now being reframed as an opportunity. (Also Read: What is ESG Score and How It Is Calculated)

Climate vulnerability is accelerating urgency. 2024 was recorded as the hottest year in the Arab region’s history, intensifying evapotranspiration, reducing groundwater recharge, and compressing already narrow growing windows. Against this backdrop, the environmental (E) component of ESG is not a compliance checkbox for Saudi agribusinesses — it is existential.

The Vision 2030 National Food Security Strategy targets raising domestic food production self-sufficiency from roughly 20% to 40% by 2030. Achieving this without dramatically improving the sustainability of land and water use is arithmetically impossible. That is precisely where ESG-aligned investment frameworks and carbon credit mechanisms are stepping in.

Saudi Arabia’s Carbon Market Architecture: What’s Been Built

Before examining agriculture specifically, it is worth understanding the carbon infrastructure Saudi Arabia has constructed — because agriculture’s entry into carbon markets depends entirely on that foundation.

In 2022, the Public Investment Fund (PIF) and the Saudi Exchange (Tadawul) co-established the Regional Voluntary Carbon Market Company (RVCMC) — the first voluntary carbon exchange in the Middle East and North Africa. RVCMC held its inaugural auction in Riyadh in November 2022, offering one million tonnes of international carbon credits. By 2023, it sold 2.2 million metric tonnes in Kenya, and in November 2024, it launched a dedicated voluntary carbon credit exchange platform at COP29 — featuring 2.5 million credits certified by Verra, Gold Standard, and Puro.earth.

In parallel, the government introduced the Greenhouse Gas Crediting and Offsetting Mechanism (GCOM) in 2023 — a voluntary, project-based domestic crediting scheme covering all sectors, including agriculture. Under GCOM, companies can register carbon reduction or removal projects, issue credits, and use them to offset emissions or monetise them commercially. A formal carbon exchange is expected to launch by late 2026 or 2027, with Xpansiv selected as the technology infrastructure provider.

KEY MARKET FIGURE

Saudi Arabia’s voluntary carbon credit market is projected to grow from USD 21.7 million (2023) to USD 124.6 million by 2030 — a CAGR of 28.3%. Agriculture has significant potential to capture a meaningful share of this growth.

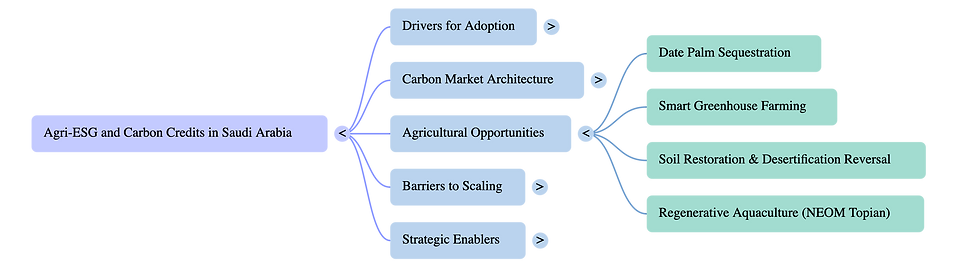

What Agri-ESG Looks Like on Saudi Soil

Agricultural carbon credits are generated by farming practices that either sequester carbon from the atmosphere or reduce emissions compared to a business-as-usual baseline. In global markets, these include soil carbon sequestration, reduced tillage, cover cropping, agroforestry, biochar application, and methane capture from livestock operations. Saudi Arabia’s agricultural profile creates both limitations and distinctive opportunities.

Date Palm Cultivation: Saudi Arabia accounts for roughly 15% of global date production. Date palms — perennial, deep-rooted, and long-lived — have meaningful carbon sequestration characteristics. A structured methodology for quantifying and verifying palm grove carbon stocks could make Saudi date orchards registrable under voluntary carbon standards.

Protected Agriculture & Smart Greenhouse Farming: Greenhouses now span more than 1,500 hectares of Saudi Arabia's agricultural land. By utilizing renewable energy and precision drip irrigation, these systems can earn credits for reducing emissions and enhancing water-use efficiency, both of which are gaining importance in ESG frameworks.

Soil Restoration & Desertification Reversal: By the end of 2024, the Saudi Green Initiative will have planted more than 115 million trees and restored 118,000 hectares of degraded land. This effort presents an opportunity to formalize land-use carbon accounting into large-scale, creditable carbon removals.

NEOM’s Topian: NEOM’s food company is pioneering regenerative aquaculture and climate-resilient farming in the north of the Kingdom, potentially becoming a demonstration project for carbon-positive agrifood production in arid geographies.

Barriers to Scaling Agri Carbon Credits in Saudi Arabia

Despite the tailwinds, scaling is not automatic. Several structural challenges need to be addressed:

MRV Infrastructure: Measurement, Reporting and Verification for agriculture in arid environments lacks validated methodology. Without rigorous MRV, credits from Saudi farmland risk credibility challenges in international markets.

Smallholder Fragmentation: Carbon project registration typically favours large, well-documented operations. Aggregation models — where multiple small farms pool to meet registration thresholds — require facilitation infrastructure that does not yet exist at scale in Saudi Arabia.

Water–Carbon Co-Accounting: Agricultural carbon sequestration relying on energy-intensive desalinated irrigation requires lifecycle accounting that captures upstream emissions. Without this, credits risk becoming misleading.

Market Literacy: Many Saudi farm operators remain unaware of GCOM registration pathways, voluntary carbon standards, or how ESG performance translates into blended finance or concessional credit access.

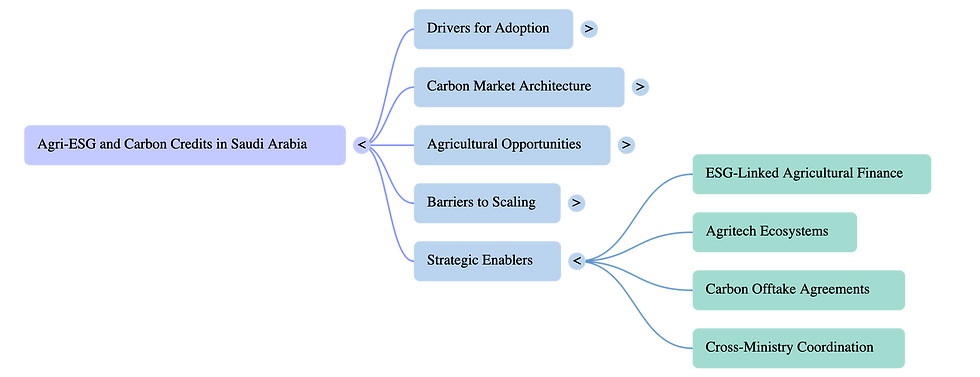

The Convergence Opportunity: ESG Finance Meets Food Strategy

What makes the next three to five years particularly significant is the convergence of multiple favourable forces. Saudi Vision 2030 is channelling billions into agricultural transformation. PIF’s SALIC subsidiary is investing across global agribusiness value chains while building domestic agritech ecosystems. International agritech companies from the Netherlands, Spain, and China have opened regional offices in the Kingdom, bringing precision agriculture, soil monitoring, and smart irrigation technologies that double as carbon data infrastructure.

The Agricultural Development Fund offers subsidised financing to farmers. If ESG metrics — including carbon credit generation capacity — are formally integrated into lending criteria, it would create a powerful incentive structure for adoption. Globally, long-term carbon offtake agreements are proving transformative. NEOM’s Enowa recently secured a commitment for 30 million tonnes of carbon credits by 2030. If analogous agricultural offtake frameworks are developed — linking food companies, sovereign buyers, and verified farm projects — Saudi Agri-ESG could move from pilot to systemic in a single policy cycle. (Related Post: ESG Advisory Service Consultants in Gurugram)

Looking Ahead

Saudi Arabia is not starting from scratch. The policy intent is clear, the carbon market architecture is being assembled, and the agricultural transformation agenda is generously funded. What the sector needs now is the connective tissue: validated agricultural carbon methodologies suited to arid geographies, aggregation platforms for smaller producers, ESG-linked agricultural finance products, and cross-ministry coordination between the Ministry of Environment, Water and Agriculture and the carbon market institutions.

For investors, agribusinesses, sustainability consultants, and ESG strategists with an eye on the Gulf, the Saudi Agri-ESG story is moving from aspiration to architecture. The window to shape that architecture — rather than merely adapt to it — is open right now.

About Sustaind

Sustaind is your partner for ESG intelligence, sustainability strategy, and green finance insights across South Asia and the Middle East.

Comments